Learning to manage your personal finances is the cornerstone to living a stress-free and happy life. However, in this era of fast consumption, managing your personal finances is not as easy as it once was. From saving for your retirement, paying off school loans or mortgages, to learning how to save and budget, it can be overwhelming. What are the impact of these factors on individual finances and how do they differ globally?

Debt Around the World

With continuous social, economic and technological advancements, more and more people around the world are falling into debt, causing debt to grow at a rapid pace. Though our disposable incoming is growing, the prices of products are too growing, causing personal debts to increase.

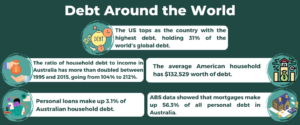

- The US tops as the country with the highest debt, holding 31% of the world’s global debt. (Visual Capitalist).

- The ratio of household debt to income in Australia has more than doubled between 1995 and 2015, going from 104% to 212%. (Finder).

- The average American household has $132,529 worth of debt. (Making Sense of Cents).

- Personal loans make up 3.1% of Australian household debt. (Finder).

- ABS data showed that mortgages make up 56.3% of all personal debt in Australia. (ABS).

The Impact of Debt

Studies show that debt is more than about money. It can have serious negative impacts on your life, leading to the breakdown of relationships, family and can lead to serious emotional and psychological issues. Debt can range from student loans, mortgage payments, credit card debt to even phone bills and rent payments.

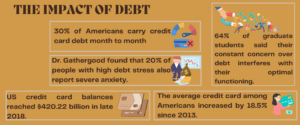

- 30% of Americans carry credit card debt month to month.

- Dr. Gathergood found that 20% of people with high debt stress also report severe anxiety. (The Simple Dollar).

- 64% of graduate students said their constant concern over debt interferes with their optimal functioning. (The Simple Dollar).

- The average credit card among Americans increased by 18.5% since 2013. (Federal Reserve Bank of New York).

- US credit card balances reached $420.22 billion in late 2018. (Nerd Wallet).

Budgeting

Budgeting is an essential tool to having good and stable personal finances. The assurance of always having money for personal needs, including food, bills and emergency situations can lift a great deal of stress off your shoulders. However, whilst budgeting is an essential tool, many people may not afford to budget their income.

- Only 1 in 3 Americans have a household budget. (Gallup).

- 20% of Americans do not save any of their annual income at all. (CNBC)

- Individuals who make less than $75,000 annually are less likely to budget than those who do. (Debt).

- 2/3 of Americans would struggle to scrounge up $1000 in an emergency. (Invested Wallet).

- 85% of Australians do not know their monthly spending amount. (Money Mag).

Saving Money

In today’s uncertain economy, it can be hard to know when you may extra money for something. One of the best ways to ensure healthy personal finances is to accumulate savings. Studies also show that the security and comfort of a savings account can lead to increased happiness.

- The average savings target is $11,234 for an Australian. (Money Smart).

- The average Australian family spends between $282 – $332 a week on groceries (Source).

- 56% of millennials do not have any money saved in their retirement accounts. (PurePoint Financial).

- The Average American saves less than 5% of their disposable income. (LA Times).

- ½ of American households currently live pay check to pay check. (invested Wallet).

- A big factor that stops many Australians from saving is mortgage stress. 45% of households contribute 30% or more of their disposable incomes towards repayments. (Savings).

Struggles of Financial Freedom

Having healthy personal finances is not easy. Often, many individuals find themselves breaking their financial resolution due to having to fork out money for an emergency, lack will power or setting unachievable goals. And without a budget or savings account, this could easily send someone into debt.

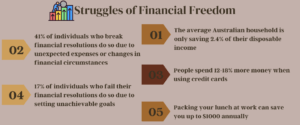

- The average Australian household is only saving 2.4% of their disposable income. (Savings).

- 41% of individuals who break financial resolutions do so due to unexpected expenses or changes in financial circumstances. (Money Smart).

- People spend 12-18% more money when using credit cards. (Purpose Generation).

- 17% of individuals who fail their financial resolutions do so due to setting unachievable goals. (Money Smart).

- Packing your lunch at work can save you up to $1000 annually. (Purpose Generation).

Financial Literacy

Lack of financial literacy can lead to many individuals to make poor financial decisions, including not knowing how to budget, or save, taking out too many credit cards or loans. These may result in debt and cause detrimental consequences.

- According to the National Endowment for Financial Education, only 24% of millennials demonstrate basic financial literacy. (Invested Wallet).

- 64% of Australian adults are financially literate. (CBHS).

- 54% of millennials expressed worry that they would not be able to pay back student loans. (PwC).

- In a survey conducted by the National Financial Educators Council, 5.2% reported that they had been turned down from a job due to lack of financial knowledge. (Financial Educators Council).

- Australia ranks 9th in the world for financial literacy. (CBHS).